There are many headlines out there that claim we’re reverting to a more normal real estate market. That would indicate the housing market is returning to the pre-pandemic numbers we saw from 2015-2019. But that’s not happening. The market is still extremely vibrant as demand is still strong even while housing supply is slowly returning.

Here’s the definition of normal from the Merriam-Webster Dictionary:

“conforming to a type, standard, or regular pattern: characterized by that which is considered usual, typical, or routine.”

Using this definition, here are five housing industry metrics that prove we’re nowhere near normal.

1. Mortgage Rates

If we look at the 30-year mortgage rate chronicled by Freddie Mac, we can see the average rates by decade:

- 1970s: 8.86%

- 1980s: 12.7%

- 1990s: 8.12%

- 2000s: 6.29%

- 2010s: 4.09%

Today, the average mortgage rate stands at 2.87%, which is very close to the historic low.

Currently, mortgage rates are anything but usual, typical, or routine.

2. Home Price Appreciation

According to Black Knight, a housing data and analytics company, the average annual appreciation on residential real estate prices since 1995 has been 4.14%.

According to the latest forecast from the National Association of Realtors (NAR), home price appreciation will hit 14.1% this year, which will be greater than any year since Black Knight began collecting this data.

Currently, home price appreciation is anything but usual, typical, or routine.

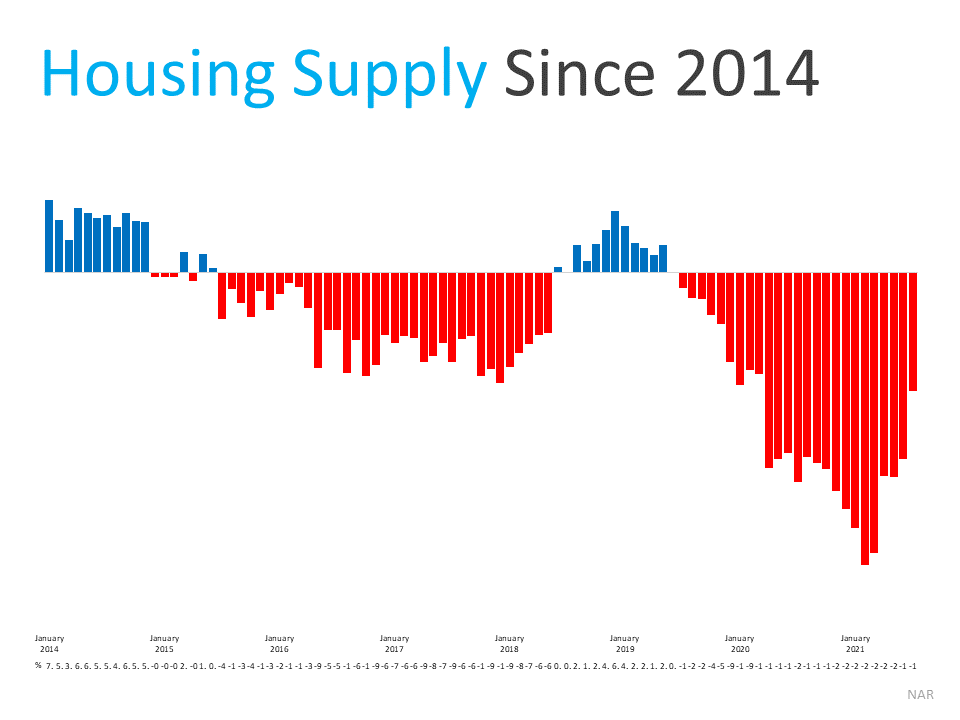

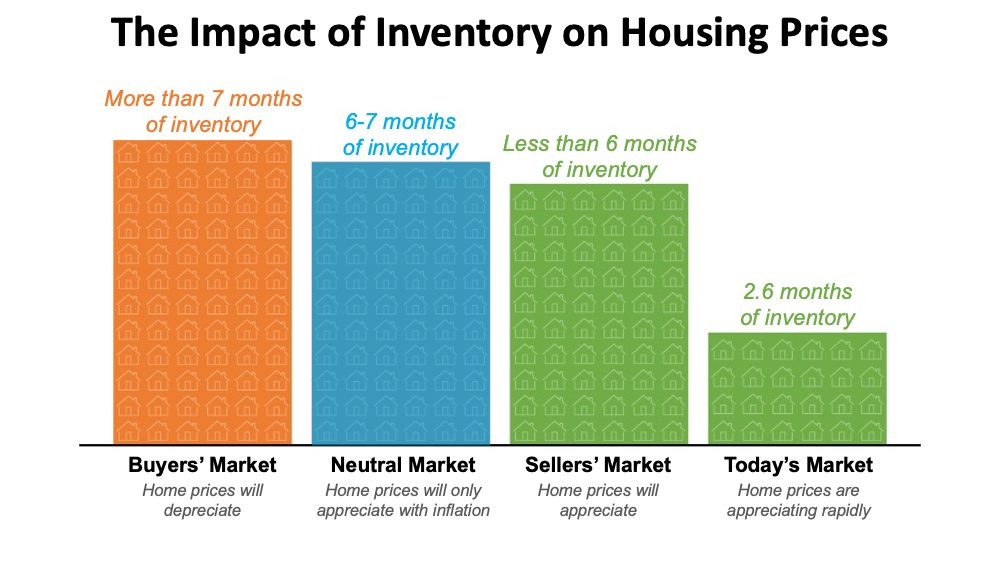

3. Months’ Supply of Inventory (Homes for Sale)

According to NAR:

“Months’ supply refers to the number of months it would take for the current inventory of homes on the market to sell given the current sales pace. Historically, six months of supply is associated with moderate price appreciation, and a lower level of months’ supply tends to push prices up more rapidly.”

As of the latest Existing Homes Sales Report from NAR, the current months’ supply of inventory stands at 2.6. That’s less than half of a normal supply.

Currently, the supply of homes for sale is anything but usual, typical, or routine.

4. Days It Takes To Sell a Home

The days-on-market metric gives an indication of how hot a market is and how quickly homes are selling. In 2019, prior to the pandemic, the average days on market stood at 35, according to NAR. Today, that number is cut in half and is now at 17 days.

Currently, the days-on-market metric is anything but usual, typical, or routine.

5. Number of Offers per Listing

According to NAR, the number of offers per listing stood at 2.2 in 2019. Today, that number is double at 4.5.

Currently, the number of offers per listing is anything but usual, typical, or routine.

Bottom Line

When…

- Mortgage rates are near historic lows

- Price appreciation is at historic highs

- Housing inventory is less than half of the normal amount

- The time it takes to sell a home is cut in half, and

- There are twice as many offers on each house

…it’s hard to say we’re in a normal market.

![Your Checklist To Get Ready To Sell [INFOGRAPHIC] | Simplifying The Market](https://eringarnerlv.com/wp-content/uploads/2021/08/20210827-KCM-Share-549x300-1.png)

![Your Checklist To Get Ready To Sell [INFOGRAPHIC] | Simplifying The Market](https://eringarnerlv.com/wp-content/uploads/2021/08/20210827-MEM.png)

![Sellers Are in a Sweet Spot [INFOGRAPHIC] | Simplifying The Market](https://eringarnerlv.com/wp-content/uploads/2021/08/20210813-KCM-Share-549x300-1.png)

![Sellers Are in a Sweet Spot [INFOGRAPHIC] | Simplifying The Market](https://eringarnerlv.com/wp-content/uploads/2021/08/20210806-MEM-1.png)